Research Article Open Access

Making Economic Social Decisions for Improving Occupational Health A Predictive Cost-Benefit Analysis

Mahmoud Rezagholi1* and Apostolos Bantekas2

1Department of Occupational and Public Health Sciences, University of Gävle, SE-801 76 Gävle, Sweden

2Department of Business and Economic Studies, University of Gävle, SE-801 76 Gävle, Sweden

- *Corresponding Author:

- Rezagholi M

Department of Occupational and Public Health Sciences

University of Gävle, SE-801 76 Gävle, Sweden

Tel: +46(0)26645093

E-mail: madrei@hig.se

Received date: November 19, 2015 Accepted date: December 22, 2015 Published date: December 29, 2015

Citation: Rezagholi M, Bantekas A (2015) Making Economic Social Decisions for Improving Occupational Health – A Predictive Cost-Benefit Analysis. Occup Med Health Aff 3:225. doi: 10.4172/2329-6879.1000225

Copyright: © 2015 Rezagholi M, et al. This is an open-access article distributed under the terms of the Creative Commons Attribution License, which permits unrestricted use, distribution, and reproduction in any medium, provided the original author and source are credited.

Visit for more related articles at Occupational Medicine & Health Affairs

Abstract

The few studies attempting to estimate costs of work-related disorders suffer from poor applied methodologies. Further, as the costs are often limited to the company, decisions about investment in improving the work environment are made at the company level. However, economic decisions on changing work environments and improving occupational health need to be made at the societal level. In an economic social decision, all direct and indirect costs imposed on society by work-related disorders are considered, regardless of who pays which cost. This study introduces and demonstrates a methodology appropriate for economic decisions at the societal level for preventing work-related disorders and promoting occupational health in the workplace. The methodology uses the concept of human capital in assessing productivity loss associated with the disorders. The empirical results show that Swedish society could have gained up to 442 855 537 SEK by preventing work-related disorders at the Swedish company Sandvik Materials Technology during 2014, 87% of which would have been captured by the company.

Keywords

Work environment; Risk factors; Absenteeism; Work capacity; Illness-related costs; Economic evaluation

Introduction

Costs of work-related disorders

A well-functioning work environment is an important factor in the production of goods and services; it improves the performance of human capital and thus organisational production. The work environment must therefore undergo regular intervention and maintenance. Failures in the work environment can lead to the development of disorders that are costly to society at both micro and macro level; for workers and firms as well as for social insurance and government. Some of the social costs are direct, such as medical costs related to the disorders, and these costs are the one most commonly in focus [1-3]. However, the costs are not limited to the direct costs; the indirect costs related to labour productivity, work quality, and all stakeholders’ potential losses are estimated to be higher [3-8]. Today, there are very few studies attempting to model the total costs including direct and indirect costs, and those that do exist have poor methodologies. However, the estimated costs do provide a basis for assessing the expected benefits of an investment for improving work environment and occupational health. An economic evaluation of intervention programs for occupational health and safety (OHS) would not be successful as long as the costs are unknown. Any decision on these programs can only be made under great uncertainty, and an incorrect decision could be expected to generate even higher costs to society. A rational decision on a proposed OHS intervention program can only be made by balancing its costs and expected benefits.

Balancing costs and benefits

Despite the low number and low quality of the existing studies, economic evaluation of intervention programs in occupational life is recognized in the relevant literature as an important input to decisionmaking [9-12]. The economic evaluation can easily be performed using the approach of cost-benefit analysis (CBA). This approach, as an economic evaluation methodology, has been successfully developed and applied in economic decision-making concerning implementation of proposed programs at government level. CBA is aimed at supporting rationality in decisions about proposed programs that have implications for the use of limited resources. Since the scientific literature recommends CBA when evaluating regulatory policies, it ought to be employed for evaluating regulatory programs devoted to improving the work environment. That is, OHS intervention programs should only be approved if they have a positive net benefit (B – C; the present value of all benefits less that of all costs) or a benefit-cost-ratio (B/C, which shows the magnitude of benefit the intervention program will produce for each unit of cost) exceeding one. If C is greater than B for a proposed program, the program may be rejected. If C is equal to B, then the existing intangible costs associated with work-related disorders are decisive. The amount of government grants and the approach of employers’ “willingness to pay” should not be the sole criterion for decision-making regarding an appropriate OHS intervention.

To make a decision on improving the work environment, the returns associated with an investment in the work environment, or the comparative benefits of alternative OHS interventions, must be traded off with their costs according to economic theories underlying the cost-output relationship. Utility in cost-utility analysis (CUA) and effectiveness in cost-effectiveness analysis (CEA) are not in monetary terms and cannot be directly compared with the intervention costs, and economic outcome is also omitted in the approach of cost- minimization analysis (CMA). Hence, CBA is preferred in an economic decision-making situation. This key analytical tool highlights the importance of assessing the expected economic outcomes of designs to change the work environment, rather than simply focusing on the cost of implementing an OHS intervention as in CMA.

Societal perspective

When assessing an OHS improvement, a CBA should have a societal perspective since the whole society pays for work-related disorders which occur in an industry. CBA in a societal perspective considers all costs and benefits experienced by all stakeholders, irrespective of who pays or gains, while a company-based CBA will ensure that the company’s intervention costs are lower than its own costs of workrelated disorders. The costs of work-related disorders and the benefits of an OHS intervention are allocated across time and among different stakeholders. An intervention program acceptable for implementation frequently requires costs, but it simultaneously generates benefits over time as the costs of work-related disorders are saved not only for the firm but also for workers and for other parties in society: public and private insurance schemes, the government, and the workers’ family and friends. The social benefits of an OHS intervention are related to the social costs of work-related disorders, which in principle are difficult to measure. However, value judgements cannot be ignored when making economic social decisions (i.e. decisions in which the costs and benefits are estimated from a societal perspective) for a proposed intervention program. The choice is only whether to make these assessments more explicitly and less implicitly, or vice versa. Further, economists are interested in the opportunity costs of rejecting an appropriate OHS intervention program rather than its financial costs. The essential burden is not about the corresponding financial costs being calculated, but rather the consequences of giving up the decision to improve the work environment. Regarding the assessment of costs related to the work environment, there are instruments available to capture some costs of implementing OHS interventions and work-related disorders [13,14].

Procedure of CBA

The first step in a comprehensive work environmental study is to identify the key elements and issues such as economic activity, occupational groups, usual exposures and disorders in the workplace, and then sickness absenteeism and presenteeism (working despite impairments). The assessment of the incremental impacts of a proposed OHS intervention is then a wider area to research. When using economic decision theory, the focus of interest is the economic costs and benefits of the intervention.

CBA for decision-making about OHS intervention programs has four common characteristics: 1) only the benefits that can be measured in monetary terms are to be included, 2) both costs and benefits are measured by market prices, 3) the inflation-adjusted market rate of interest is used for discounting the annual net benefit stream, and 4) the main constraints are usually the company’s budget constraints (economic burden), the manager’s behaviour and valuations, and the activity’s nature and status in the market. For a societal predictive CBA, the scope is wider and the time horizon may be longer. The CBA should include all tangible costs and benefits, irrespective of whether they are private or social, direct or indirect. When the costs and benefits are equal, the intangible costs are considered for a rough estimate.

Benefits associated with changes in the work environment are given by the standard principles of welfare economics. The expected benefits are related to disease-related costs that can also affect the employers’ willingness to pay for improving the work environment. OHS intervention costs consist of financial costs (expenditures) and economic depreciation of resources in use, plus the forgone interest as an opportunity cost.

Sometimes, alternative proposals for changing the work environment are put forward, with different costs and different effects on labour productivity depending on their priorities and efforts. Among all acceptable and feasible designs that improve the work environment, the design that should be chosen is the one that maximizes net benefits and/or the benefit-cost-ratio, while still fulfilling any constraints. Thus, the maximization of net benefits is topical when several options differing in costs and/or effects are available. The CBA, in this case, should demonstrate not only that the benefits exceed the costs (i.e. a positive net benefit), but also that the excess of benefits over costs (i.e. the economic efficiency associated with a proposal) is maximized subject to constraints.

Inputs to an OHS-related CBA

Economic evaluations of occupational health interventions are usually based on partial studies of the work environment. They focus on certain ergonomically- and/or physically-oriented interventions in workplaces [7,8,15-19], and pay little attention to the psychosocial environment in terms of policy, leadership and organisation. However, it is difficult to disentangle the causes and impacts of work-related disorders for each dimension of the work environment, and a CBAbased decision based on a partial study of the work environment may be wrong if, for instance, the costs include only those due to a physical exposure while the benefits are included for all exposures. Economic evaluations of partial OHS interventions can only be successful with good knowledge of the socio-economic impacts of each specific exposure, and the surety that other exposures remain unchanged during each partial exposure analysis. Otherwise, when all missed and unproductive working hours are assumed to be caused by a single exposure, the economic impact of reducing the risk factor may be dramatically overestimated. Although the importance of psychosocial exposures such as mental stress, few breaks, low pay, low status and poor supervision has been acknowledged [20], in addition to physical and ergonomic risk factors, epidemics of specific diseases have often forced researchers to address specific exposures [13,15,19,21-25]. In addition to the partial nature of many studies of occupational exposure, there are poor methodologies and omitted inputs in occupational CBA. Despite studies attempting to identify and assess productivity loss due to sickness absenteeism and/or presenteeism [6-8,14,22,24,26,27], the applied models are undeveloped. Further, inputs to CBA are limited to certain explicit costs, such as productivity loss in the workplace. A number of studies have also covered some implicit sources of costs and benefits, but most of them applied CBA to a specific disease [13,15], or only provided a theoretical framework [9]. Two other concepts should also be considered in the cost calculations: the concept of opportunity cost (i.e. the costs associated with opportunities that are forgone when the resources are not put to their highest-value alternative use) and the concept of market prices. The main costs to be identified in making an economic decision on improving occupational health are the costs of the intervention, and the illness-related costs on which the anticipated benefits of implementing the intervention are based.

Intervention costs: The total intervention costs are mainly divided into two groups: a) the cost of performing a work environmental study including the cost of developing an appropriate OHS intervention program to supply to the decision maker, and b) the cost of changes in the work environment according to the program in order to prevent work-related disorders and improve occupational health. Any government grants should not have a negative sign in a CBA at the societal level, as the contribution is a social cost paid by taxpayers. The intervention costs should not include medical care expenditures as a cost to be recovered.

Illness-related costs: The total costs of work-related disorders can be classified as the potential income loss and the medical care expenditures for treatment and rehabilitation of ill workers. There are also economic and non-economic costs associated with work-related disorders that refer substantially to social and human welfare, such as non-market labour productivity (i.e. reduced household productivity and leisure activities) and reduction in quality of life and life expectancy. However, it is difficult to assess some of these in monetary terms; that is, they are intangible costs.

The benefits of an OHS intervention consist of the resulting changes in illness-related costs, which have two important sources:

(a) Direct illness-related costs, which mainly comprise medical care expenditures including expenses for treatment and rehabilitation such as visits to doctors and other practitioners, pharmaceuticals, and hospitalisation, plus transportation costs. The direct illness-related costs should be distinguished from the company’s investment costs to prevent work-related disorders and improve health. Direct illnessrelated costs are the costs that will be reduced as a result of the investment.

Different countries have different rules for paying compensation to the ill worker over time and by any party for chronic illness or partial disability. The specific rules should be considered in calculating these costs, which are usually distributed between worker, employer, and the public sector. These rules should also be considered in assessing the government’s reduced tax revenues. The intangible costs here are related, for instance, to the victim’s family, the consequences of disorders for the victim and society, and the firm’s circumstances.

(b) The indirect illness-related costs mostly refer to the potential income loss when 1) illness leads to absenteeism, 2) unskilled and/or inexperienced workers with low productivity replace absent workers, 3) ill workers continue to work with reduced work capacity (presenteeism), and 4) healthy skilled workers take over absent workers’ tasks, which can result in overtime payments, decreased labour productivity, and overload that may increase the risk of illness and thus future absenteeism and presenteeism. The last of these is an intangible long-term effect.

Labour productivity is not only affected by human capital factors such as competence and experience, but also by the psychosocial [6], ergonomic, and physical work environment [7,8]. Researchers in the field have paid great attention to the indirect illness-related costs, despite poor and obscure methodologies [10,19,20,28-30]. The costs are about costs associated with lost working hours and impaired work ability caused by work-related disorders. Thus, sickness absenteeism and presenteeism are two main sources of labour productivity loss. The expected social benefits of OHS intervention programs are directly related to the reduction of absenteeism and presenteeism. The productivity loss may be several times greater than the direct illnessrelated costs, and furthermore, ill but present workers who are working at a reduced capacity may account for a larger proportion of productivity loss than actually absent workers [14,27,30]. In the long run, impairment is related to future sickness absenteeism [31,32], which makes it even more costly.

Many researchers in the field argue that the productivity loss of sickness absences might be limited due to the company’s “elasticity”, because people are not 100% efficient and some of the work might be performed by the already available work force without additional costs [33]. This argument, however, ignores the opportunity costs of resources, and also the fact that these companies already suffer from low productivity due to failures in the organisational work environment. In attempting to replace the absent workers’ job tasks with “available labour”, companies often end up increasing the amount of labour because the new and inexperienced workers need education and training. However, in principle, labour productivity decreases as the amount of labour increases while the output remains unchanged.

The estimation of productivity loss is, of course, more complicated than the estimation of health-related direct costs. There are three measurement methods which are usually discussed and/or applied for assessing labour productivity loss: the human capital approach (HCA), which involve a societal perspective in assessing the forgone revenue; the friction cost approach (FCA), which is really a firm-level cost estimation method; and the subjective inward method or willingness to pay (WTP), which is based on decision makers’ interests, valuations, and behaviour. WTP can also be used to assess the intangible costs associated with work-related disorders. The availability/feasibility and validity/reliability of these measurement instruments have been widely discussed [14]. HCA is a salary-based method and is consistent with the economic theory that in perfectly competitive labour market, wages should reflect workers’ marginal contributions to a firm’s output.

Accordingly, lost productivity is equal to lost earnings. FCA is based on the cost of countermeasures used by employers to deal with sickness absenteeism and presenteeism. The firms may have redundant staff to compensate for absences, or they may hire temporary workers or offer overtime payments to their employees in order to reach the predetermined level of production. The cost of these countermeasures has been used by profit-maximizing firms to approximate the productivity loss. WTP and FCA do not require detailed individuallevel data on exposures, disorders, and their impacts on absenteeism and presenteeism; but they lack a societal perspective, especially in the long run. In a firm-level CBA, the long-term benefits of improving the work environment are mostly captured by workers, while the improvement has no long-term effect on the firm’s output. However, a program that reduces the number of lost working hours not only increases the utility of the paid workers by increasing leisure [26], but also increases the firm’s competiveness and future income by ensuring a good long-term position in the market.

The indirect illness-related costs are not limited to the labour productivity loss at work. The company’s flexibility and social capital, the quality of the goods and services produced, the security of the firm’s market position, delivery liability, and the workers’ home productivity can be dramatically affected by increased diseases in the company. The public sector is also affected by work-related disorders in an industry.

Time effect: The final input in CBA refers to differential timing concerning the cost components in an OHS intervention, as costs and benefits that occur at very different points in time cannot be compared. All such costs should be adjusted for inflation and discounted at a given interest rate to estimate their present value. Discounting enables rational decision-making by capturing the net present value (NPV) expected of the OHS intervention. The aspect of discount rate in CBA is due to the fact that in a market economy people prefer to make payments later and receive benefits sooner; present consumption is thus valued against future consumption. In particular, any comparison of net present value of alternative interventions with different time horizons must include this adjustment if the comparison analysis is to be valid.

Purpose

The purpose of the present study was to conduct an underlying costbenefit analysis for rational decision-making prior to an occupational health intervention in the Swedish company Sandvik Materials Technology. The cost-benefit analysis was performed with a societal perspective.

Methodology

Data collection procedure

The data required for this study were collected from Sandvik Materials Technology (SMT). Data on medical costs and efforts to prevent disorders and promote occupational health were collected from the company’s health service, while information about the characteristics of the jobs and workers and information about different occupational exposures and their effects on lost working hours was collected via a questionnaire administered to the workers in April 2015.

A total of 22 risk factors were considered: 14 psychosocial (conflicts; insults; harassment; bullying; alienation; discrimination; stress over high requirements; stress over unclear expectations; and problems with salary, authority, job security, status, stability, and gratitude), 3 ergonomic (handling heavy objects, repetitiveness, and body postures), and 5 physical (problems with air quality, temperature, noise, lighting, and vibration).

The workers were asked to assess the risk factors, their lost and unproductive working time, and whether failures in the work environment affected their sickness absenteeism and presenteeism. Participation was voluntary, but was encouraged by the company’s safety unit.

To avoid missing and confusing answers, the participants answered the questions in their workplaces with paper and pencil while the supervisor was in attendance. Responses from every party were anonymous to each other, and forwarded to the researchers only. The results of the study were then presented to the company. Important sources of social costs associated with work-related disorders were identified and assessed as described below:

Health-related direct costs: The total direct costs of illness (DC) consisted of 1) medical care expenditures (ME) as the amount of money paid for hospitalisations, medications, and also visits to nurses, doctors, and therapists; and 2) transportation expenditures (TE). The total expenditures paid by all stakeholders during 2014 were estimated as:

DC =MEW+MEE+MEP+TE, (1)

where W, E, and P stand for worker, employer, and public sector, respectively. Hence DC also included non-work-related illness.

Health-related indirect costs (potential income loss): These costs were related to the opportunities forgone by SMT due to sickness absenteeism and presenteeism during the last year. Absenteeism was measured by asking respondents how much work time they missed because of disorders. Measurement of presenteeism was more complex, and so several instruments were used to capture it in the questionnaire. These instruments were based on the concepts of perceived impairment at work, work quality, potential work capacity, and workers’ employment rate. Employees were also asked how much any failures in the work environment hindered them from performing their ordinary tasks in leisure, at home, and in meeting job demands.

The potential income loss was expressed as the product of illnessrelated missed working time multiplied by national median wages, as actual salaries could have been correlated with missed working time and low quality products. The original HCA was developed and adjusted to the specific properties of production in SMT (i.e. interdependences between work tasks in team production) as well as the state of the Swedish labour market in terms of unemployment and market failures leading to allocative inefficiency (deadweight losses).

The rate of interdependence was based on the replacement ability for an employee and the time sensitivity of an employee’s work. This, along with the rates of unemployment and monopsony power, was used to assess the marginal revenue product of labour (MRPL), which is a product of marginal revenue (MR) or equivalency, the market price of the firm’s product (p), and the marginal product of labour (MPL). An isolated job in SMT would have a multiplier of 1, while a more demanding job would have a higher multiplier.

The indirect cost of sickness absenteeism of a worker during 2014 (APL) was estimated on the basis of the worker’s potential contribution to the firm’s output per hour ( MRPL /h ):

APL=Ah.MRPL/h=Ah.(1+r).(wh) (2)

where wh is equal to the national hourly wage; r is the result of rates for interdependence, unemployment, and monopsony power; and Ah is the number of hours of sickness absence during 2014.

The cost of impairments during 2014 (WPL) was also estimated on the basis of L/h MRP ,multiplied by the number of scheduled working hours minus the total number of sickness absence hours (Ph) and the rate of impairment at work (α):

WPL=Ph.α.MRPL/h=Ph.α.(1+r).(wh) (3)

Hence, APL and WPL assess labour productivity loss due to sickness absenteeism and presenteeism, respectively.

The Swedish social insurance agency pays the sick absent worker 80% of their wage from their fifteenth sick day, to compensate for wages. The payments (SIC) were estimated for the year as:

SIC=0.8.(wh.Ahfrom 15th sickness day) (4)

There is an additional cost to society; the so-called tax revenue loss (TRL), which consists of the income taxes not received from the sick absent worker who has received compensation less than their wages. The cost was estimated based on the wage, the tax rate (30%), and the difference between wages and compensation as follows:

TRL=0.3. [(1-0.8).(wh.Ah)] (5)

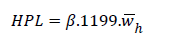

Work-related home productivity loss (HPL) was estimated for each ill worker during the year as follows:

(6)

(6)

Where, β is the rate of reduction in home productivity due to failures in the work environment, 1199 is the estimated number of hours per year that each individual devoted to work in the home according to Statistics Sweden (SCB), and h w is the estimated (unpaid) average hourly wage for different work at home based on market prices.

Thus, the total social cost of work-related disorders for each worker in SMT during 2014 (TSCw), including both actual costs and potential income loss, was estimated as:

TSCw=DC+APL+WPL+SIC+TRL+HPL (7)

Finally, the costs were estimated for SMT’s 3500 employees to assess the total social costs of work-related disorders in the company, E(TSC) , which is equal to the maximum social benefits expected by eliminating failures in the SMT’s work environment, E(MSB) :

Where, kA and kP represent the degree of sickness absences and reduced work capacity that were caused by the work environment, respectively.

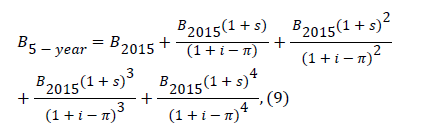

Adjusting for differential timing

The assessment of time-profile costs of work-related disorders should be consistent with the investment costs for improving the work environment. Some of the costs are incurred during a certain time, while others might be allocated across a period of several years. In this case, the depreciation year of the equipment and furniture to be purchased for changing the work environment is decisive for the longitude of estimating the expected net benefits of the investment. Thus, a decision to implement a proposed OHS intervention program must require the net present benefit (NPB) to be positive. The present value of MSB in eliminating work-related disorders at SMT was estimated along five years as:

Where, i, π, and s stand for rates of interest, inflation, and annual increase in salaries, respectively.

Results

The empirical results of applying the above-described methodologies at SMT during 2014 are presented in the following tables. All costs are in SEK and rounded to integers. EUR and USD to SEK exchange rates as of 15 October 2015 were 9.30 and 8.12, respectively. As shown in Table 1, more than 28% of the absenteeism indirect cost was assessed as being work-related; that is, due to insufficiencies in the work environment.

| Average missed working hours | Total missed working hours | Rate of sickness absence (%) | Indirect cost of sickness absenteeism | Indirect cost of work-related sickness absenteeism |

| 101.84 | 356 457 | 5.7 | 216 668 647 | 61 073 580 |

Table 1: Absenteeism: missed working hours and their indirect costs (labour productivity loss).

As expected, the cost of sickness presenteeism was much larger than the indirect cost of sickness absenteeism. Further, a greater proportion of the cost was work-related; about 41% (Table 2).

| Average rate of impairment at work | Average unproductive working hours | Total unproductive working hours | Cost of presenteeism | Cost of work-related presenteeism |

| 21.58 | 363.53 | 1 272 354.29 | 786 129 476 | 322 731 058 |

Table 2: Presenteeism: unproductive working hours and their costs (labour productivity loss).

As shown in Table 3, reduced labour productivity in SMT during 2014 cost the company 383 804 638 SEK – a huge potential income loss due to the existence of work-related disorders in the workplace.

| Average missed and unproductive working hours | Total missed and unproductive working hours | Total work-related missed and unproductive working hours | Work-related productivity loss |

| 465.37 | 1 628 811 | 461 102.62 | 383 804 638 |

Table 3: Lost working hours due to sickness absenteeism and presenteeism.

The illness-related costs for SMT consisted of medical costs and labour productivity loss (Table 4).

| Direct medical costs | 33 848 654 |

| Labour productivity loss at work due to sickness absenteeism | 216 668 647 |

| Labour productivity loss at work due to sickness presenteeism | 786 129 476 |

| Home productivity loss due to the disorders | 141 051 189 |

| Payments by the Social Insurance Agency from the fifteenth sick day | 38 801 991 |

| Tax revenue loss | 6 613 976 |

| Total illness-related costs for Swedish society (Social Value of Occupational Health) |

1 223 113 933 |

| Total illness-related costs for SMT (Organisational Value of Occupational Health) |

1 036 646 777 |

Table 4: Estimated costs of workers’ disorders at the societal level.

The total social costs of work-related illness mean that Swedish society could have expected benefits of up to 442 855 537 SEK by improving the work environment at SMT during 2014 (Table 5).

| Direct medical costs | 8 953 646 |

| Labour productivity loss at work due to absenteeism | 61 073580 |

| Labour productivity loss at work due to presenteeism | 322 731 058 |

| Home productivity loss due to work-related disorders | 38 083 821 |

| Payments by the Social Insurance Agency from the fifteenth sick day | 10 263 903 |

| Tax revenue loss | 1 749 529 |

| Total social costs of work-related disorders | 442 855 537 |

Table 5: Estimated costs of work-related disorders at the societal level.

| Direct medical costs | 750 140 |

| Labour productivity loss due to sickness absenteeism | 61 073 580 |

| Labour productivity loss due to sickness presenteeism | 322 731 058 |

| Total cost of work-related disorders for SMT | 384 554 778 |

| Investment costs of preventing disorders and improving health | 6 932 165 |

Table 6: Estimated costs of work-related disorders for SMT compared to the company’s investment in the work environment.

A comparison of Tables 4 and 5 shows that most (87%) of the social benefits due to the absence of work-related disorders would be captured by SMT.

Assuming a five-year depreciation for the new furniture and equipment purchased in order to improve the work environment, the related time profile benefits would be expected to be 1 981 539 754 SEK for society and 1 720 666 372 SEK for the company, according to (9). The time profile benefits can guide decision makers as to the level of profitable investment in improving the work environment. This economic decision, which will be taken by SMT’s management, is about the new investment in the work environment for next year with the aim of saving as much cost as possible. In economic decision analysis of alternative intervention programs, the costs of these programs would be compared with their expected benefits. Hence, the time profile benefits will be multiplied by the rate of the programs’ abilities to reduce work-related disorders, and then reduced by the present value of five-year investment costs estimated in the same way. The new intervention programs should consider risk factors in the work environment.

Table 7 presents the various environmental deficiencies mentioned by the employees who answered the questionnaire, arranged in order of priority for investment in the work environment to prevent disorders and promote occupational health.

| Psychosocial risk factors | Physical risk factors | Ergonomic risk factors |

| Stress over unclear expectations | Low air quality | Awkward body postures |

| Stress over high requirements (job demands) | Noise | Monotony |

| Instability (constant changes) | Improper temperature | Handling heavy objects |

| Low status | Vibration | |

| Conflicts | Dissatisfactory lighting | |

| Low salary/reward | ||

| Job insecurity | ||

| Alienation | ||

| Ingratitude | ||

| Discrimination | ||

| Low authority | ||

| Insults | ||

| Bullying | ||

| Harassment |

Table 7: The priority for investment in the work environment based on workers’ judgments.

Discussion

The effect of non-work-related exposures on the organisational value of occupational health

In attempts to perform a predictive CBA which is as reliable as possible, we assumed that the costs of work-related disorders were caused by work-related exposures in three main groups: the psychosocial, ergonomic, and physical work environment. However, SMT cannot be isolated from Swedish society in exposure studies and health affairs, and some costs could be due to factors that are not directly related to the workplace. It is incredibly difficult to find out, for instance, the extent to which the misuse of alcohol, drugs, and tobacco, or diseases like migraine and depression – all of which affect the costs – are really due to deficiencies in the work environment. On the other hand, there was no other way in our study than to estimate the costs based on the employees’ judgements of occupational exposures and their effects on their ill health and impairments. Thus, in terms of illness-related costs, the comprehensive estimate has higher certainty than the partial estimate (i.e. estimation of the costs of work-related disorders).

The problem with presenteeism measurement

There were both difficulties and uncertainties with the measurement of sickness presenteeism. There is no way to directly measure a worker’s work capacity or to determine a standard work capacity. Employees’ judgments are subjectively different, due to differences in their individual characteristics. On the other hand, the quantity and quality of production as demanded by profit-maximizing firms may be too high, and ever-fluctuating depending on the state of the market and the positional war between the company and its competitors. Thus, several instruments were used to capture presenteeism in this study. For instance, the assessment of work capacities based on job demands was mitigated by workers’ judgments. However, like the concept of health, work capacity needs to be defined in a multidimensional and contextual way so that it can be encompassed in each activity. Depending on the tasks and the environmental factors behind the impairments, in some cases workers with reduced work capacity can perform the same task as workers with full work capacity.

Limitations of the predictive CBA

There are some limitations in the predictive CBA of future investments for improving the work environment in SMT. The CBA occurred before approval, and not after the implementation of an OHS intervention and the achievement of its economic outcomes. A CBA performed before choosing an intervention is aimed at ensuring an effective intervention and a profitable investment in the work environment, while a CBA performed after implementing the intervention is aimed at ensuring that the intervention has been effective and the investment justified. Thus, the following should be kept in mind when making economic decisions about the work environment:

1) The CBA was performed in Sweden, and so care should be taken when applying this model to other countries with different social security systems, health care, labour market, and so on.

2) Identification of the sources of benefits was the most challenging issue in the CBA. It was not possible to evaluate all benefits to human welfare in economic terms. Examples of the non-monetary benefits include ecological gains and improved quality of life and life expectancy.

3) The predictive CBA provides guidance for economic decisionmaking at the societal level, but is not a complete system; other determinants, both economic and non-economic, must be taken into account in the decision-making. One example of a relevant economic determinant is the budget constraint for the safety unit, while relevant non-economic determinants include the management’s valuations and preferences.

4) We assumed that the patterns and impacts of the exposures, as well as all the micro- and macroeconomic factors such as the rate of economic growth, the technological trend, and the states of the markets, were constant during the analysis. This is likely an unrealistic assumption if the analysis is run for the long term. Thus, uncertainty is inherent in our time profile assessments of benefits.

Evaluation of instruments to assess productivity loss

The assessment of labour productivity losses in this study was based on the concept of human capital, as introduced by Schultz (1960) and Becker (1987). This concept encompasses work ability, knowledge, skills, and health; all the potential forces and capabilities embodied in humans that lead to creation of individual and social well-being [34]. It is a useful concept for capturing productivity losses from a societal perspective, and can easily be augmented by adding important determinants such as the state of the labour market. Three instruments have been developed to assess the amount of labour productivity loss when considering the economics of work environment and occupational health, each based on either the forgone opportunities and potential income loss (as in the HCA), or the related actual costs and the employer’s behaviour (so-called inward instruments). The inward instruments are divided into an objective method based on frictional period and countermeasures (FCA), and a subjective method based on the employer’s own valuations (WTP). While economists are interested in HCA, many researchers in the field lean towards the objective inward method, FCA.

The subjective inward method, WTP, is used for making business decisions with respect to affordability and willingness: “I would pay 5 million dollars to a contractor who can raise my employees’ productivity by 20%”. It is not a reliable estimator, but it is related to the economic concept of consumer surplus; that is, the difference between what consumers are willing to pay for the good or service and what they actually pay for it. This method can also be used to value the intangible costs associated with work-related disorders. Since the amount of WTP depends on the imagined size of the direct and indirect disease-related costs, it can be easy to use in decision-making without needing to collect individual data.

Many researchers in the field argue that HCA overestimates the true absence-related productivity losses, because short-term absences might be compensated with greater effort or unpaid overtime while longerterm absences would lead to replacement of workers with new hires. These researchers also propose that FCA aims at estimating only the actual lost production (or the cost of replacing sick workers by formerly unemployed workers to keep the company’s predetermined production level) instead of potential lost income during the “friction period” (the time taken to replace ill workers and achieve the company’s goal) [9,12,14]. Koopmanschap et al. [12] even suggest that FCA should be multiplied by a coefficient of 0.8, suggesting that the productivity loss is 80% of the friction costs of absenteeism. This method often drastically underestimates the true labour productivity loss, and is also inconsistent with standard economic theories concerning opportunity cost and profit-maximizing firms. It is true that the human capital method estimates the potential income loss, and not the current cost of maintaining the predetermined level of production during frictional periods. However, when unemployment in society is higher than the frictional level in the workplace, the replacement cost is low and hence FCA underestimates the true labour productivity loss caused by work-related disorders. The opportunity cost of labour is near to zero in societies with unemployment, because in this case the labour market can supply workers who are satisfied with minimum wage to replace those who are absent due to illness. Further, the anticipated benefits of implementing an effective OHS intervention program are related to the opportunity cost of not implementing the program. FCA is identical to HCA only in cases of full employment and a perfectly competitive labour market, when the high opportunity costs of labour and incremental salaries for overtime work prevail.

The idea of estimating the costs of maintaining the level of production during frictional times by using the available labour (countermeasures for sickness absenteeism and presenteeism) ignores several facts. Firstly, overloading the existing labour force increases the risk of disease and thus the future disease-related costs. Secondly, replacement with unskilled workers increases the required working hours due to education, training, extra staffing, and so on, which certainly decreases labour productivity. Thirdly, economic impacts are not limited to the company, but the approach completely ignores the effect of work-related disorders on other stakeholders. The short-term approach of frictional costs is only relevant for the employer, and not at all for the surrounding society. Fourthly, unhealthy workers reduce not only the quantity of production but also the quality of the goods and services produced. The reduced quality is reflected in the price of the product and thereby the salary. This is usually ignored in FCA. Fifthly, FCA is not able to account for the medium- and long-term effects of sickness absenteeism and presenteeism on either the company, the market, or the economy as a whole. Finally, although the diseaserelated productivity loss is observed in society, it can be hidden at the company level; the frictional cost for short-term illness (up to one week) is close to zero for the company, due to unpaid production (forced labour), and is zero for long-term illness when the ill worker is replaced by somebody else.

The gross benefits are mostly distributed between employers, employees, and the public sector. The long-run benefits from reduced productivity loss are mostly captured by the employees via obtaining higher wages [26] in competitive labour markets and mostly captured by the employers in unemployment and non-competitive labour markets by getting sustainable status in the market while paying wages much lower than the marginal revenue product of labour because of the workers’ low bargaining power. Society captures the long-run benefits by obtaining a sustainable economic development and a high growth rate.

The original HCA also has two major limitations. Firstly, it assumes that the national economy has a perfectly competitive labour market and full employment. Thus, the equilibrium price of labour determined by market forces and profit maximization is conditioned to be equal to the marginal revenue product of labour. However, at least two conditions should be met for this equity. The first is the possibility of equal job opportunities, and the second is the existence of “same salary for the same job”. Further, if there is less than full employment, the reservation wage (minimum acceptable wage), which is less than the marginal revenue product of labour, is usually paid. In our adjusted HCA, the average wage for each competence is estimated at the national rate in order to reflect differences in terms of labour productivity and to see the status of the labour market. Otherwise, the individual wage could depend on the worker’s health status and could also vary between different gender, ethnic, and age groups.

The second major limitation of the original HCA is that, although the approach is appropriate for workers performing discrete tasks in isolation, it fails to take into account the interdependent ties between the work functions in a company with team production [26]. Finding a perfect substitute for an absent worker is often more difficult and expensive in modern production. When production takes place in a team, the absence of a member affects the marginal product of the whole team, and the cost of this absence is really equal to the cost of maintaining the team’s target output. In order to maintain the target, the remaining members in the team can be paid overtime, but only if the absent competence is not unique. In our team-specific HCA, the entire productivity of the team was considered.

Our adjusted team-specific HCA ignored non-economic consequences such as leisure and life quality (indicators of human welfare). However, the non-economic human costs of pain and suffering, and reductions in life quality and life expectancy, were intangible costs in our CBA. Further, the macro-economic issues (e.g. fluctuations in unemployment, inflation, and economic growth) are still intangible to estimate but are certainly affected by increased workrelated disorders. Thus, the claim that the original HCA may overestimate the true productivity loss is not at all realistic in view of the many non-measurable but definite economic and non-economic consequences that have been omitted even in the adjusted HCA. The omission of these factors means that the expected social benefits of preventing health-related productivity losses are larger than the average wage on which the model is based.

Conclusions

Employees’ ill health and reduced work capacity in SMT was mostly caused by factors such as stress over unclear expectations and high requirements, instability, low air quality, noise, improper temperature, and awkward body postures at work. Of the total illness-related social cost, 36% was due to the work environment. Swedish society could have benefitted by up to 442 855 537 SEK in improving the work environment at SMT during 2014, 87% of which would have been captured by the company.

The medical costs of work-related disorders were a small proportion of the total cost. The largest source of cost was the productivity loss, which accounted for 99.8% of the total cost for SMT and 95.3% of the total cost for Swedish society. Reduction in work capacity, mostly caused by the psychosocial work environment, was the largest source of the costs due to work-related disorders: 84% of the total cost for SMT and 81% of the total cost for Swedish society.

Acknowledgments

The authors gratefully acknowledge the Faculty of Health and Occupational Studies at the University of Gävle-Sweden and the Swedish company Sandvik Materials Technology, for their support and cooperation in writing this article.

References

- Lubeck DP (2003) The costs of musculoskeletal disorders: Health needs assessment and health economics. Best Practice & Res ClinRheumatol 17: 529-539.

- Punnett L, Wegman DH (2004) Work-related musculoskeletal disorders: The epidemiologic evidence and the debate. J ElectromyogrKinesiol 14: 13-23

- Piedrahita H (2006) Costs of work-related musculoskeletal disorders (MSDs) in developing countries: Colombia case. Int J OccupSafErgon 12: 379-386.

- Eklund JA (1995) Relationships between ergonomics and quality in assembly work. ApplErgon 26: 15-20.

- Maniadakis N, Gray A (2000) The economic burden of back pain in the UK. Pain 84: 95-103.

- Taiwo AS (2010) The influence of work environment on workers productivity: A case of selected oil and gas industry in Lagos, Nigeria. Afr J Bus Manag 4: 299-307.

- Hameed A, Amjad S (2009) Impact of office design on employees’ productivity: A case study of banking organizations of Abbottabad, Pakistan. J Pub Affairs Admin Manag 3: 1-13.

- Sehgal S (2012) Relationship between work environment and productivity. Int J Eng Res Appl 2: 1992-1995.

- Van Dongen JM, Van Wier MF, Tompa E, Bongers PM and Van der Beek AJ, et al. (2014) Trial-based economic evaluations in occupational health: Principles, methods, and recommendations. J Occup Environ Med 56: 563-572.

- Uegaki K, de Bruijne MC, Lambeek L, Anema JR, Van der Beek AJ, et al. (2010) Economic evaluations of occupational health interventions from a corporate perspective – a systematic review of methodological quality. Scand J Work Environ Health 36: 273-288.

- Tompa E, Culyer AJ, Dolinschi R (2008) Economic evaluation of interventions for occupational health and safety: Developing good practice.

- Koopmanschap MA, Rutten FFH, Van Ineveld BM, Van Roijen L (1995) The friction cost method for measuring indirect costs of disease. J Health Econ 14: 171-189.

- Meijster T, Van Duuren-Stuurman B, Heederik D, Houba R, Koningsveld E, et al. (2011) Cost-benefit analysis in occupational health: A comparison of intervention scenario for occupational asthma and rhinitis among bakery workers. Occup Environ Med 68: 739-745.

- Mattke S, Balakrishnan A, Bergamo G, Newberry SJ (2007) A review of methods to measure health-related productivity loss. Am J Manag Care 13: 211-217.

- Lahiri S, Gold J, Levenstein C (2005) Net-cost model for workplace interventions. J Safety Res 36: 241-255.

- Tompa E, Dolinschi R, Oliveira C, Amick BC 3rd, Irvin E (2010) A systematic review of workplace ergonomic interventions with economic analyses. J OccupRehabil 20: 220-234.

- Beevis D, Slade IM (2003) Ergonomics – costs and benefits. ApplErgon 34: 413-418.

- Goggins RW, Spielholz P, Nothstein GL (2008) Estimating the effectiveness of ergonomics interventions through case studies: Implications for predictive cost-benefit analysis. J Safety Res 39: 339-344.

- Goossens ME, Evers SM, Vlaeyen JW, Rutten-van Mölken MP, Van der Linden SM (1999) Principles of economic evaluations for interventions of chronic musculoskeletal pain. Eur J Pain 3: 343-353.

- Oxenburgh M, Marlow P (2005) Computer-based cost benefit analysis model for the economic assessment of occupational health and safety interventions in the workplace. J Safety res 36: 209-214.

- Evanoff B, Kymes S (2010) Modelling the cost–benefit of nerve conduction studies in pre-employment screening for carpal tunnel syndrome. Scand J Work Environ Health 36: 299-304.

- Ungar WJ, Coyte PC (2000) Measuring productivity loss days in asthma patients. Health Econ 9: 37-46.

- Rappaport H, Bonthapally V (2012) The direct expenditures and indirect costs associated with treating asthma in the United States. J Allerg& Therapy 3: 1-8.

- Lamb CE, Ratner PH, Johnson CE, Ambegaonkar AJ, Joshi AV, et al. (2006) Economic impact of workplace productivity losses due to allergic rhinitis compared with select medical conditions in the United States from an employer perspective. Cur Med Res Opin 22: 1203-1210.

- Reenen HH, Proper KI, Van den Berg M (2012) Worksite mental health interventions: A systematic review of economic evaluations. Occup Environ Med. 69: 837-845.

- Pauly MV, Nicholson S, Xu J, Polsky D, Danzon PM, et al. (2002) A general model of the impact of absenteeism on employers and employees. Health Econ 11: 221-231.

- Goetzel RZ, Long SR, Ozminkowski RJ, Hawkins K, Wang S, et al. (2004) Health, absence, disability, and presenteeism cost estimates of certain physical and mental health conditions affecting U.S. employers. J Occup Environ Med 46: 398-412.

- Tompa E, Dolinschi R, de Oliveira C (2006) Practice and potential of economic evaluation of workplace-based interventions for occupational health and safety. J OccupRehabil 16: 375-400.

- Boles M, Pelletier B, Lynch W (2004) The relationship between health risks and work productivity. J Occup Environ Med 46: 737-745.

- Pelletier B, Boles M, Lynch W (2004) Change in health risks and work productivity over time. J Occup Environ Med 46: 746-754.

- Bergström G, Bodin L, Hagberg G, Aronsson G, Josephson M (2009) Sickness presenteeism today, sickness absenteeism tomorrow? A prospective study on sickness presenteeism and future sickness absenteeism. J Occup Environ Med 51: 629-638.

- Hanssen CD, Andersen JH (2009) Sick at work - a risk factor for long-run sickness absence at a later date. J Epidemiol Community Health 63: 397-402.

- Lahiri S, Levenstein C, Nelson DL, Rosenberg B (2005) The cost effectiveness of occupational health interventions: Prevention of silicosis. Am J Industrial Med 48: 503-514.

- OECD (2001) The well-being of nations: The role of human and social capital. OECD Publishing, Paris.

Relevant Topics

- Child Health Education

- Construction Safety

- Dental Health Education

- Holistic Health Education

- Industrial Hygiene

- Nursing Health Education

- Occupational and Environmental Medicine

- Occupational Dermatitis

- Occupational Disorders

- Occupational Exposures

- Occupational Medicine

- Occupational Physical Therapy

- Occupational Rehabilitation

- Occupational Standards

- Occupational Therapist Practice

- Occupational Therapy

- Occupational Therapy Devices & Market Analysis

- Occupational Toxicology

- Oral Health Education

- Paediatric Occupational Therapy

- Perinatal Mental Health

- Pleural Mesothelioma

- Recreation Therapy

- Sensory Integration Therapy

- Workplace Safety & Stress

- Workplace Safety Culture

Recommended Journals

Article Tools

Article Usage

- Total views: 11839

- [From(publication date):

December-2015 - Apr 04, 2025] - Breakdown by view type

- HTML page views : 10853

- PDF downloads : 986